Q: Are REITs (real estate investment trusts) going to be hurt by the new tax reform?

Not at all. In fact, the new tax plan actually favors these generous dividend payers.

Let me explain why – and then point you towards the best REITs to buy for 2018.

A Smaller Tax Bill on REIT Dividends

The IRS already allows REITs to avoid paying income taxes if they pay out most of their earnings to shareholders. As a result these firms tend to collect rent checks, pay their bills and send most of the rest of the cash to us as dividends.

But the IRS considers the dividends you and I receive from our REITs “non-qualified” dividends. This means they are taxed at our regular income rate (which today is as high as 39.6% at the federal level).

Until now, that is. REIT investors will benefit from the tax breaks that “pass through” businesses will receive in the new code. Investors will be allowed deduct 20% of their REIT dividend income, which means their current 39.6% tax bill will drop to 29.6% (according to The Wall Street Journal and Nareit).

Interestingly, REIT income would be taxed at a lower rate than regular rental income (which would not receive the deduction). Which means if you don’t have a burning desire to change light bulbs and play landlord yourself, it will be cost-effective to simply sit back, make a few clicks and buy real estate stocks instead of physical properties!

The REIT sector will also dodge what looked like a problematic new requirement – a rule limiting the deductibility of interest payments for “highly indebted businesses.” (Rumors of this had already roiled the high yield bond market.)

REITs often rely on debt to expand and grow their portfolios. Fortunately for their investors, they are getting a “hall pass” in the new tax code – they’ll still be allowed to deduct their debt’s interest payments.

This means we have the “all clear” to continue playing Monopoly with our retirement portfolios in buying these growing dividend streams. As usual, there are more compelling buys (and yields) than others. We’ll discuss the best opportunities for 2018 in a minute – first, let’s talk about the “stay aways.”

Avoid These REITs At All Costs

Now stick with me, because we’re going to indulge our contrarian streak even more by not doing what most “first-level” investors would immediately do after reading this: run out and buy the Vanguard REIT ETF (VNQ).

To start, even though its 4% payout looks appealing, it’s only half of what we’d need to fuel our 8% yield—and keep our no-withdrawal strategy chugging along.

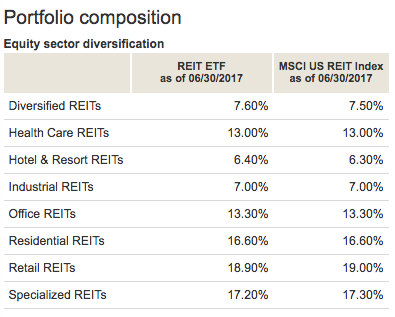

But that’s not the main reason why I’m worried about VNQ. I’m far more concerned about the ticking time bomb planted in its portfolio. See if you can spot it:

Source: Vanguard

The problem is in the second line from the bottom: 18.9% of VNQ’s holdings are retail REITs – its largest allocation, and the worst REITs you could own right now.

That 18.9% is sitting right in the path of Amazon.com (AMZN), which is eating retailers like Macy’s (M), L Brands (LB) and Guess (GES) alive! If these chains are in permanent trouble (I’d argue they are), that’s a big problem for their landlords.

I don’t know about you, but I wouldn’t want to bet a penny of my retirement cash against Amazon “disrupter-in-chief” Jeff Bezos. That’s why I’ve set the retail REIT exposure in my “8% No-Withdrawal Retirement Portfolio” at 0%.

Instead, we’re going to focus on REITs who are already raising their rents without any problem. Their higher and higher cash flows will help assure we’re not settling for the “mere” 8% total returns that their generous current yields would suggest.

The Secret to Safe 20%+ Yearly Returns From REITs

When selecting REITs, you should focus on FFO growth. This single metric is what drives dividend gains (which in turn are the single factor that drive stock prices higher).

Funds from operations (FFO) represents the amount of cash a REIT actually generates from its operations. It’s where our dividend originates – which makes it the building block for everything else in the REIT world.

If FFO is stagnant, a firm can only increase its payout by increasing its payout ratio. And this isn’t sustainable over time.

Rising FFO on a per share basis, on the other hand, will basically force management to raise its dividend. And that’s what ultimately drives the stock price higher, because dividend growth is all that matters for REITs. Figure out where the dividend is going, and you know where the stock price is heading.

Combine 10%+ dividend growth with high-single-digit current yields, and you have a formula for safe 20%+ annual gains from REITs. With a significant portion of that coming as cash dividends.

For example, let’s take blue chip healthcare landlord Ventas (VTR). The firm has steadily raised its dividend this decade, and its stock price has followed its payout higher:

Ventas’ Stock Price Rises With Payout

This happens because Ventas, give or take a point, tends to pay a 5% current yield:

Ventas Pays 5%, More or Less

Which means, as Ventas raises its dividend, investors are willing to pay more for its now-higher payout. So the price rises in tandem.

Of course there’s a third way to win with REITs – buy them cheap, and wait for their valuations to appreciate. You could have achieved outsized gains with Ventas by buying (or adding to) a position when the stock paid more than 5.3% or so – an indicator that its price was low.

And while Ventas looks about fairly priced today, there are bargains trading for less than 10-times their funds from operations (FFO) today and yielding 8%, 9% and even 10%!

Now that’s cheap. And it means their investors will enjoy additional upside when their yields and valuations eventually “normalize” as late-arriving first-level investors bid their share prices higher.

My 2 Favorite Growth REITs: 7% to 10% Cash Yields Plus 20%+ Yearly Price Upside

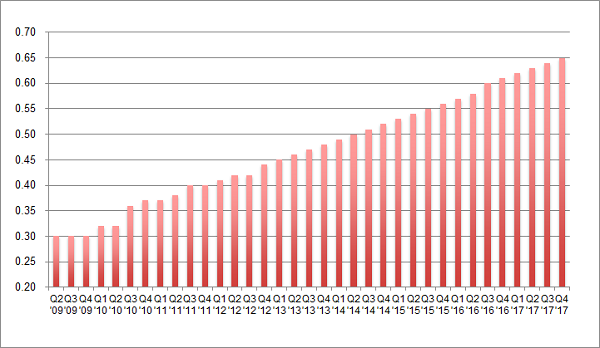

My favorite REIT today recently raised its dividend again by 4% over last quarter’s payout. This marks the 21st consecutive quarterly dividend hike for the firm:

Dividend Hikes Every Quarter

It pays a 9.4% yield today – but that’s actually a 10% forward yield when you consider we’re going to see four more dividend increases over the next year. And the stock is trading for less than 10-times FFO. Now that’s cheap.

However I expect its valuation and stock price will rise by 25% over the next 12 months as more money comes stampeding into its REIT sector. Which makes right now the best time to buy and secure a 10% forward yield.

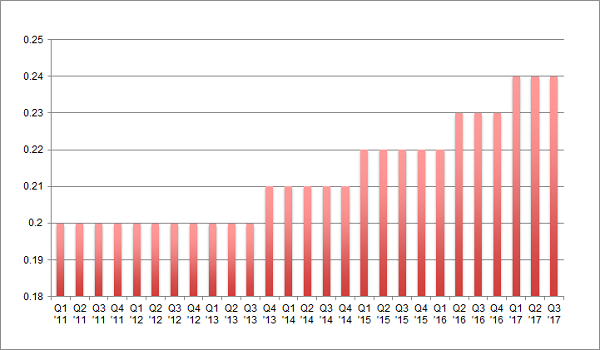

Same for another REIT favorite of mine, a 7.1% payer backed by an unstoppable demographic trend that will deliver growing dividends for the next 30 years.

The firm’s investors have enjoyed 20% dividend growth in recent years. And right now is actually a better time than ever to buy because its growing base of assets is generating higher and higher cash flows, powering an accelerating dividend:

An Accelerating Dividend

This stock should be owned by any serious dividend investor for three simple reasons:

- It’s recession-proof,

- It yields a fat (and secure) 7.1%, and

- Its dividend increases are actually accelerating.

These two REITs are both “best buys” in my 8% No Withdrawal Portfolio – an 8% dividend paying portfolio that lets retirees live on secure payouts alone. And they can even enjoy price upside to boot, thanks to the bargain prices they’re buying at.

And thanks to the new new tax plan, there’s never been a better time to buy REITs and live off their dividends. But it’s important to choose wisely.

Retail REITs are dangerous (with the entire industry in a death spiral), while other recession-proof issues are bargains. I’d love to share the latter with you – including specific stock names, tickers and buy prices. Click here and I’ll send my full 8% No Withdrawal Portfolio research you to right now.

Recent Comments