If you’re worried that stocks are expensive again, well, they are. The current bull market is making a run at history. But it’s also costly to stay in cash (and lock in zero income). Fortunately, it’s possible to buy some downside protection with yield.

I understand the “I’m worried so I’m sitting in cash” concern. And I know many investors who continue to sit on their money and hope for a big pullback. But wouldn’t it be nicer to bank 32% total returns with 8%, 9% or even 10% or more of it coming as dividends?

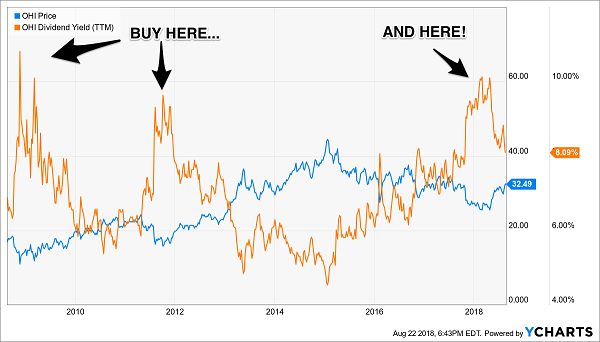

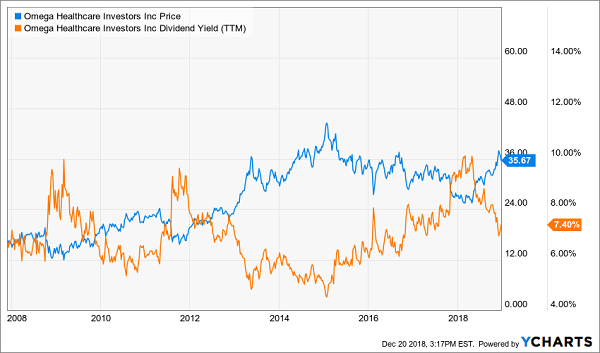

Our Contrarian Income Report subscribers who smartly stayed with Omega Healthcare Investors (OHI) – a big paying REIT – have done much better than their scared cash hoarder friends, as well as the broader market in general. Last year actually started inauspiciously as OHI announced a dividend “freeze.” The stock slipped. But a freeze isn’t the same as a cut – and OHI’s payout was well covered by its funds from operations (“FFO” – more on why this matters shortly).

The misunderstanding would soon be our gain, as the stock yielded 10% (thanks to years of previous dividend hikes). And anytime that OHI has paid double-digits in the past, it marked a major bottom for the stock. So why would this time be any different?

OHI’s Dividend Limits Its Price Downside

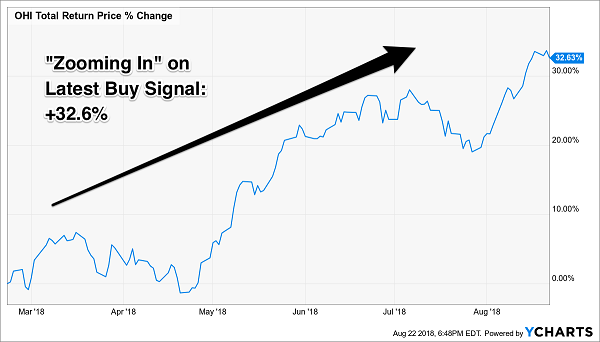

Let’s “zoom in” to see how OHI rallied off its most recent double-digit high to return 32% including dividends!

Better Than Cash – A Big Yield with Upside

Secure yields are the truly the “rubber duckies” of the investing world. Mr. Market can push them underwater for a period of time, but eventually, they rocket up to the surface.

With that in mind, let’s “zig” a zagging stock market by discussing three high paying mutual funds. Big dividends plus a human at the wheel – that’s my idea of a bear-proof payout-powered portfolio.

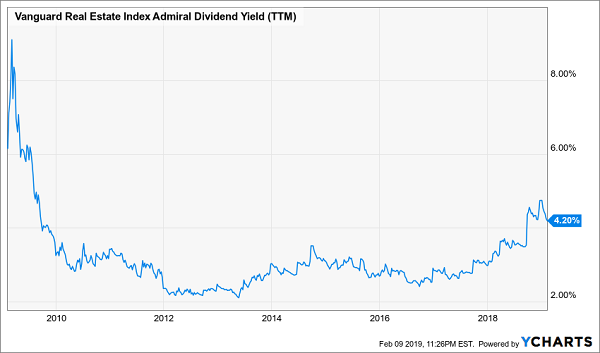

Vanguard Real Estate Index (VGSLX)

Type: REIT (real estate investment trusts)

Assets Under Management: $59 billion

Yield: 4.2%

Expenses: 0.12%

At a yield of just more than 4%, the Vanguard Real Estate Index (VGSLX) – which has a twin fund, the Vanguard Real Estate ETF (VNQ) – isn’t knocking the socks off high-income investors. But VGSLX actually is one of the best-yielding equity mutual funds in the game.

In fact, most of the top mutual funds for equity income are invested in real estate investment trusts (REITs). No surprise there. REITs are naturally income-friendly thanks to their mandate to redistribute 90% or more of their taxable income back to you and me as dividends. Better still, REITs were shackled in 2018, helping to drive up yields to their highest point in roughly a decade!

VGSLX Hasn’t Yielded This Much Since the 2007-09 Bear Market!

Vanguard’s indexed REIT fund is weighted by market cap, so the fund is filled with blue chips such as communications-infrastructure play American Tower (AMT), mall operator Simon Property Group (SPG) and logistics REIT Prologis (PLD).

It’s a worthy fund that has served its shareholders well since inception in 2001, and it does allow investors to keep almost all of their returns with a cheap expense ratio. That said, if you’re looking to bundle REITs together in a fund, this is one area where active management tends to shine. In fact, several CEFs yield far more than VGSLX and have bested Vanguard’s offering over the long-term.

Let’s move on.

AB High Income (AGDAX)

Type: High-Yield Bond

Assets Under Management: $5.9 billion

Yield: 7.6%

Expenses: 0.82%*

Next up is a no-brainer in the high-yield field: junk bonds.

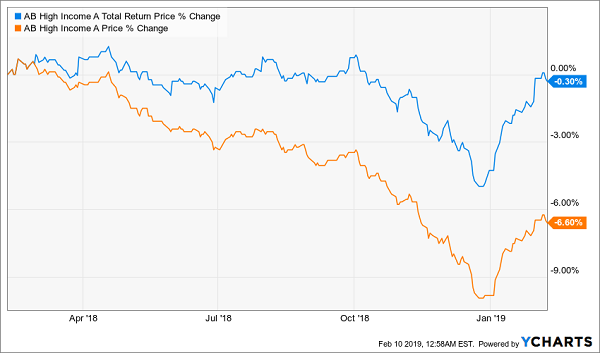

You can get plenty of yield out of just the American junk market, but AB High Income (AGDAX) takes things a step farther by breaking out its passport and delving into developed-market and emerging-market bonds, too.

AGDAX actually invests in more than just junk debt. High-yield corporates make up 44% of the fund, with another 10% in collateralized mortgage obligations, 9% in investment-grade corporates, 9% in emerging-market sovereign debt, 6% in “global governments” and the rest peppered among other types of income investments.

Of Course, Junk Has Had a Rough Go Of It Lately …

Unlike with the indexed VGSLX, AllianceBernstein’s fund has plenty of managerial brainpower to go around. Its five-manager team averages nearly 26 years of experience apiece, including 21 years apiece at AB.

But boy, is it costly. The 0.82% in annual fees isn’t all that bad – you’ll typically find that in CEFs – but what you won’t find is an additional 4.25% sales charge that AB charges for these A shares. That will cost you literally thousands if not tens of thousands of dollars over the course of your investment.

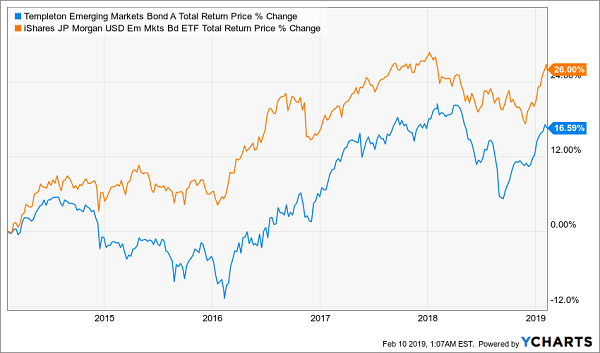

Templeton Emerging Markets Bond (FEMGX)

Type: Emerging-Markets Bond

Assets Under Management: $35.2 million

Yield: 8.6%

Expenses: 1.17%*

Emerging-market bonds are one of the highest-yielding assets you can invest in. The inherent enhanced risk of less developed countries – complete with higher levels of corruption, geopolitical risk and less regulated markets – forces sky-high yields to compensate investors for their trouble.

In the case of Templeton Emerging Markets Bond (FEMGX), you’re getting well north of 8% for that trouble, but you’re also actually putting a cap on your risk. See, FEMGX – under the managing team of Michael Hasenstab, Calvin Ho and Laura Burakreis – holds 124 different positions across a number of EMs, such as Brazil, Argentina, Ghana, Indonesia and Thailand.

Management typically wants to invest 80% of the portfolio in EM bonds, but they can use their discretion should opportunity dry up. In fact, at the moment, less than 60% of the portfolio is invested in bonds, with the rest parked in cash.

But those managerial decisions will cost you – in fact, even more than AGDAX.

These Returns Look Even Worse After Costs

FEMGX charges a steep 4.25% maximum sales charge, as well as 1.17% in annual expenses. But it doesn’t stop there. There’s also a potential 0.75% CDSC (deferred sales charge), and a 0.25% 12b-1 fee (marketing!) to swallow.

Worse …

It’s Not Even Beating the Index Fund

Management certainly earns its fees at times, but it’s hard-pressed to keep up with its own litany of charges.

I’m keeping an eye on these three funds, but I don’t think it’s time to buy them just yet. I’ve got three more high paying plays I like even better right now with great growth potential on top of their generous current yields.

The 3 Best Bear-Proof Buys (with 8%+ Dividends) Right Now

With the recent market insanity you’ve probably thought about dumping – or at least reducing – your stock holdings and focus on fixed-income investments as you near and enter retirement. It sounds like a smart move, but going lean on stocks leaves you open to two big risks:

- That you’ll outlive your savings, and

- You’ll miss out on the long-term gains only the stock market can offer.

So why not blend a portfolio of 8%+ bond funds with smart stock picks that provide you with similarly high yields with upside to boot? Sure, they may “sell off” a bit if the markets pull back. But who cares. Like a savvy rich speculator, you’ll be able to step in and buy more shares when they are cheap – without having to worry about your next capital withdrawal.

Let’s revisit healthcare landlord Omega Healthcare Industries (OHI). The firm’s payout is usually generous, and always reliable – yet, for whatever reason, its sometimes manic price action gives investors heartburn.

But it shouldn’t. It’s actually quite predictable. Check out the chart below, and you’ll notice:

- When the stock’s yield is high (orange line), its price is low. Investors should buy here.

- When the stock’s price is high (blue line), its yield is low. Investors should hold here and enjoy their dividend payments.

Investing is Easy: Buy When Yield (Orange Line) is High

Of course this simple timing strategy is much easier to employ if you don’t need stock prices to stay high to retire. Most investors who sell shares for income spend their days staring at every tick of the markets.

You can live better than this, generate more income and even enjoy more upside by employing our contrarian approach to the yield markets. We live off dividends alone. And we buy issues when they are out-of-favor (like right now) so that our payouts and upside are both maximized.

Plus 8% Dividends, Paid Monthly, Make Retirement Even Easier

And by the way, you can even use my “no withdrawal” strategy to make sure you’re:

- Banking 8% annual dividends,

- Enjoying additional price upside, and

- Getting paid monthly to boot!

If this interests you, I’d recommend starting with my all-star retirement portfolio. It contains 8 of the absolute best preferred stocks, REITs and CEFs out there.

If you’re scratching your head at these terms, you’re not alone. These are investments that you won’t hear about on CNBC or read about in the Wall Street Journal. Which is why we have these fantastic opportunities available in this “no yield” world.

I’ll explain more about them in a minute. I’ll also show you why my 8% eight-pack is well diversified across all types of investments and sectors, and the cash flows funding these dividends will do well no matter what happens in the broader economy or stock market.

Plus, as I hinted, relentless dividend growth means your 8% yield will be more like 10% in short order.

I’m ready to take you inside this “no-worry” retirement portfolio now. Click here and I’ll show you the 8 bargain investments inside it and give you their names, tickers, buy-under prices and much more.

Recent Comments