Want more yield and price upside in your portfolio? You can get both from bonds – if you think a little contrarian, of course.

Just avoid the four common mistakes most bond investors make, and you’ll probably do better than most stock jockeys!

“First-level” financial advisors tell you to sell some stocks and buy more bonds as you get older. Their reasoning is that you should be trading upside for yield and security as you go.

You could actually trade all of your stocks for bonds today and retire comfortably on as little as $500,000. If you buy the right bonds.

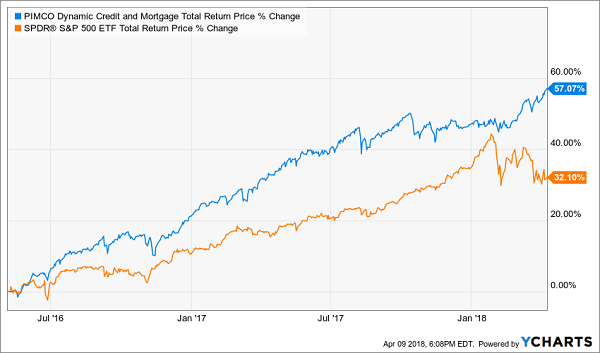

Here’s an example. In May 2016, my Contrarian Income Report subscribers bought PIMCO’s Dynamic Credit and Mortgage Fund (PCI) on my advice. It’s delivered 57% total returns (including generous dividends) in less than two years – for more upside and less drama than the broader stock market:

+57% in Two Years From Safe Bonds

Of course all bonds don’t provide these types of returns. In fact, most don’t. Why not? One or more of these four traps hold them back. Let’s start with the machines, which are quite overhyped these days.

Flaw #1: Most Bond Funds are Too Passive (and Dumb)

“Passive” investing – rule-based portfolio building – is all the rage with stocks. While we could argue their merits for equities, these methods simply don’t work well with bonds. Fixed income expertise can’t be readily pre-programmed.

Here’s the main reason why bond indexing is bad. Let’s consider stock indexes, which are weighted by company size. Generally speaking, the larger the firm, the more it matters in the index’s performance.

If you “buy by size” in the debt markets, it would be a disaster. Stock market value for indexes doesn’t include debt. But bond markets are all debt by definition. Follow the computers in Bond-ville and you’d maximize your exposure to the firms that borrow the most money!

That’s the opposite of what we’re looking for in bonds, where our goal is to maximize our “coupon” (the percentage yield) while minimizing our risk (and making sure we get paid back our principal.)

Flaw #2: Many Bonds Are Sitting Ducks When Rates Rise

The economy is as strong today as it’s been in 10 years, so it’s a safe environment for the Fed to hike rates and “taper” (or withdraw some of their cash injection from the post-2008 world).

This is bad news for safe bonds like U.S. Treasuries. What happens to the 2.8% paying 10-year Treasury if rates rally to 3.5%? Your old bond loses value, because investors prefer the new bond (with the higher paying coupon.) After all, you signed up for a decade!

This is also mixed news for for Corporate America, and the debt it issues. Corporate bonds, unlike Treasuries, have higher yields and more flexibility. This can include floating rate coupons – which means these firms must pay more on their current debt as rates rise.

But their added interest expense is our gain as income investors. We’ll take the higher payments attached to floating rate issues!

We should also take the superior yields that are nestled below an imaginary line of alleged safety.

Flaw #3: Perceived Safety is Overpriced

The best deals in the bond market are actually just below the somewhat arbitrary investment grade cutoff. It’s where savvy fund managers capitalize on the fact that pension funds, banks, and insurance company overly cautious by-laws prohibit investing in these “low quality” (according to the herd, but not to us) issues.

For example, the iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD) is the largest fund buying just what its name says – investment grade corporate bonds. It’s returned a respectable 5.38% yearly since its 2002 inception.

But you and I can do better if we find smart managers and trust them to locate deals for us that don’t quite qualify for this arbitrary criteria. Nuveen’s Preferred & Income Securities Fund (JPS), for example, doesn’t get the love it deserves even though it’s crushed LQD in recent years.

JPS has just $2 billion under management (versus $32 billion for its ETF cousin). And it has an unfair (and lazily assigned) two-star fund rating from Morningstar.

Nuveen deserves better. Its JPS fund has a similar mandate as LQD – to bank income from Corporate America. And it isn’t hamstrung by the former’s “investment grade” edict. This freedom is fantastic for our returns, as the fund pays double the dividend and has more-than-tripled up its overrated competitor over the last five years:

Perceived Safety (Blue) is Detrimental to Returns

Another problem with LQD is that you’ll never get a deal on it. Here’s why.

Flaw #4: Investors Pay Retail Price

Most ETFs (exchange traded funds) trade for the value of their assets. If you buy a bond ETF, you’re going to pay $1 for $1 worth of bonds in its portfolio. This may sound obvious, but it doesn’t have to be this way!

We can actually cherry pick our purchases to demand bargains. To do this, we’ll focus on closed-end funds (CEFs) – which can actually trade above or below the market value of their portfolios.

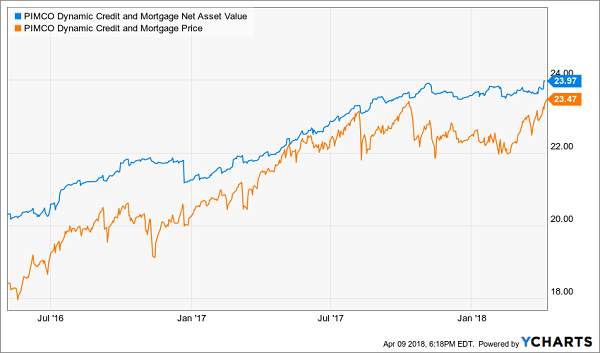

Back to PCI – when we bought it two years ago, the fund was trading for $18.42 per share. But its net asset value (NAV) was actually $20.31. Which means we picked up $1.89 per share for free!

Bargains like these don’t last forever, and PCI’s discount window has since closed. You can see this in the chart below as its price (orange line) has moved higher toward its NAV (blue line):

We Profit When Bargains End

As this sale ended, we profited directly. Our fund’s price was “pulled” higher by its NAV. (Which also continued to rise, by the way – another benefit of our prescient purchase!)

Buy Now: Monthly Dividend Superstars Paying 8%+ with 10%+ Upside

Now I’d like to introduce you to three incredible income plays most people don’t even know about.

They’re among my absolute favorite investments to keep your nest egg safe. Plus they pay a generous dividend every single month – which is especially nice because your income payments line up conveniently with your monthly bills!

All three first-class bond funds check the four contrarian boxes we outlined above:

- They’re managed by the best bond minds in the business,

- Their coupons are ticking higher as rates rise,

- Their portfolios are focused on the “sweet spot” for safety and yield, and

- They trade at generous discounts to their NAV.

In fact, the 8.7% payer I have in mind trades at a bizarre 5.3% discount to its NAV.

Meanwhile, my second favorite fund is the brainchild of the best bond manager on the planet. It pays 8.9%.

And the third fund simply mints money and pays its investors a generous 8.5% yearly distribution. Yet not 1 in 1,000 investors have heard of it!

I don’t expect these yields and discounts to last for long. The market is simply too efficient to let this “free money” sit there in these ultimate fixed income plays.

Fortunately I have a special report on these three 8%+ dividend machines prepared for you. It includes their names, tickers, and buy-up-to prices along with my full analysis. Click here and I’ll send you my special report on these monthly dividend machines (good for 8%+ yearly yields with 10%+ price upside) today.

Recent Comments