Closed-end funds (CEFs) are increasingly becoming favorites of retirees looking for income. And why not? Many pay 5%, 6% and even 7% or more today. In a world where stocks yield 2% and bonds just 3% or so, the extra dividends can be the key to a comfortable retirement.

The “closed” in CEF technically means that the fund’s pool of shares is fixed. Which is why these vehicles can have wild price swings above and below the values of their actual assets. (Good for us contrarian income seekers – we can buy below fair value to maximize our yields and upside.)

They are also closed in their actual communications with the financial world. Fund information is often limited (sometimes to one-page fact sheets) and it’s difficult to get management to talk to you.

(Also good for us contrarians – it makes bargains more prevalent in this mysterious corner of the income world. Especially for us persistent types).

But with the deals and big dividends come the dogs, and it’s up to us to piece together facts and financial crumbs of information to determine which to buy, avoid and sell. Ultimately we must look at each fund to figure out if its:

- Distribution is safe, and

- Price is stable.

The dividend is important, but it doesn’t mean much if you give the payout back on the price side. Some funds cannibalize their own capital, paying dividends while their quote ticks lower and lower. Like these 26 money losers.

CEF Trap #1: Money Losers (26 Flawed Funds to Avoid)

There are 26 CEFs, still in business and publicly traded today, that have lost money since inception. This is an impressive level of incompetence.

When these funds are formed, they buy assets so they can achieve a positive return – ideally more than their promised dividend – and pay regular distributions to their investors. They have but one job to do.

These 26 have failed at that. They haven’t made anyone any money, ever, and they are nothing more than Ponzi schemes that reach into their own investors’ pockets to pay them.

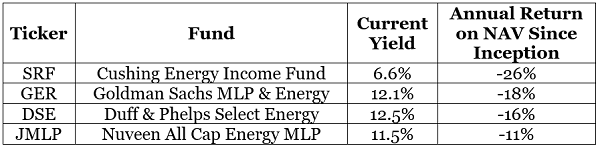

Here are the four biggest offenders which have “achieved” double-digit annual losses on their net asset values (NAVs) since inception:

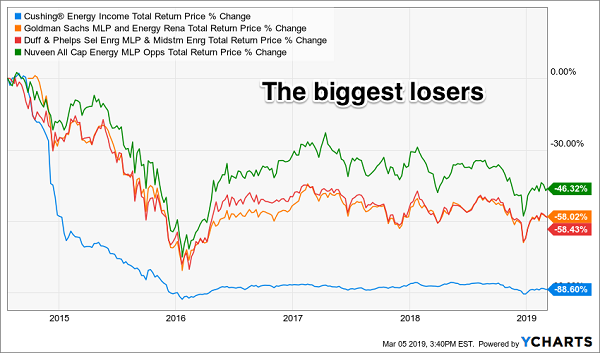

Three of these four funds launched in 2014, pinning the tail on the energy top nicely. But it’s one thing to run with the herd, and another to bankrupt it entirely – which is what the Cushing fund has somehow managed to do:

The 4 Biggest CEF Losers

But how do you know in advance when a sector is overheated and ripe for a crash? Look for premiums, which should always be faded.

CEF Trap #2: Paying a Premium (82 More Funds to Avoid)

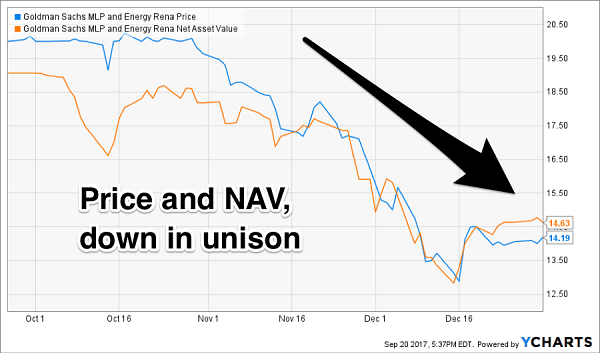

When the Goldman MLP fund launched, it traded at a steep premium (10%+) to the value of its underlying assets. In other words, investors were paying $1.10 to get a dollar into Goldman’s latest sucker bet:

The Goldman Touch

Of course, price and NAV turned south quickly, and the premium disappeared. But today there are still 82 CEFs trading for more than their assets! All should be avoided, no matter how good you think the fund is (or how many stars Morningstar gives it).

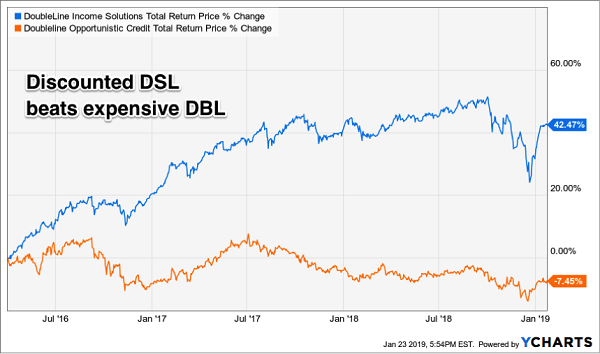

Consider the tale of “Bond God” Jeffrey Gundlach’s two funds – the DoubleLine Income Solutions Fund (DSL), which has traded at a discount to its NAV since inception, and its more popular sister fund, the DoubleLine Opportunistic Credit Fund (DBL), which has traded for a premium.

There’s no reason for the disparity. Gundlach runs both funds and has a wide mandate (the ability to buy anything he wants) with both.

Both 8%+ dividends were safe. But the price discounts (or lack thereof) made the difference, which is why I told my subscribers to purchase DSL in April 2016 and avoid DBL. Good move, because we banked quick 43% gains while DBL investors watched their cash grind sideways:

DSL Shows Why We Demand Discounts

CEF Trap #3: Not Enough Yield on NAV (& 130 More to Avoid)

Let’s circle back to the money losers, because we let a few funds off the hook too easily. Namely those that haven’t generated at least 5% yearly returns on NAV since inception.

If a manager can’t generate a 5% return on assets, how are they supposed to pay us much more than that? Sure, CEFs can borrow money for cheap and leverage their gains a bit – but even 20% leverage on 5% only gets us to 6%, the bare minimum of our income thresholds.

With this higher 5% requirement, the loser trap pool we started with in section one increases from 26 to 130 “must avoid” funds. Add in our 82 losers selling for premiums to NAV, and we have a total of 212 CEFs that we shouldn’t be buying right now.

The Solution: A “Dividends-Only” Retirement Strategy

If you’re combing around CEFs, you have the right idea. The best retirement strategy is one in which you don’t need stock prices to stay high to retire.

Most investors who sell shares for income spend their days staring at every tick of the markets. You can live better than this, generate more income and even enjoy more upside by employing our contrarian approach to the yield markets. At the Contrarian Income Report, we live off dividends alone. And we buy issues when they are out-of-favor so that our payouts and upside are both maximized.

Plus 8% Dividends, Paid Monthly, Make Retirement Even Easier

And by the way, you can even use my “no withdrawal” strategy to make sure you’re:

- Banking 8% annual dividends,

- Enjoying additional price upside, and

- Getting paid monthly to boot!

If this interests you, I’d recommend starting with my all-star retirement portfolio. It contains 8 of the absolute best preferred shares, REITs and CEFs out there.

If you’re scratching your head at these terms, you’re not alone. These are investments that you won’t hear about on CNBC or read about in the Wall Street Journal. Which is why we have these fantastic opportunities available in this “no yield” world.

Let me also show you why my 8% eight-pack is well diversified across all types of investments and sectors, and the cash flows funding these dividends will do well no matter what happens in the broader economy or stock market.

Plus, as I hinted, relentless dividend growth means your 8% yield will be more like 10% in short order.

I’m ready to take you inside this “no-worry” retirement portfolio now. Click here and I’ll show you the 8 bargain investments inside it and give you their names, tickers, buy-under prices and much more.

Recent Comments