The tax reform debate in Washington is roiling the municipal bond market—and that’s setting up a screaming buying opportunity for contrarians on the hunt for income.

I’ll tell you why, and show you exactly how to cash in, in a moment.

First, if you’ve been watching “munis” for any length of time, I probably don’t have to tell you that muni-bond investors detest uncertainty.

That’s because they’re risk-averse folks who just want a high, tax-free yield on their money.

After all, that’s what municipal bonds are for; they offer higher yields than US Treasuries; they’re untaxed for most Americans, unlike federal bonds and stock dividends; and their prices don’t fluctuate much.

Look at how the iShares National Muni Bond ETF (MUB)—the blue line in the chart below—has performed over the past decade versus the iShares 20+ Year Treasury Bond ETF (TLT), shown in red, and the SPDR S&P 500 ETF (SPY), in orange:

A Smooth Ride With Munis

Sure, your investment grew a lot more if you bought stocks or Treasuries, but you also saw wild price swings in times of uncertainty. Munis don’t do that—instead, they provide lower price returns and greater stability, which is why you see that serene, flat blue line.

This is where tax reform comes in. Specifically, it’s the debate about private activity bonds (PABs) that’s weighing on munis now.

PABs are a special form of municipal bond in which a municipality issues a bond, then lets a private company use those funds to build something that benefits the public, like a hospital or new power lines.

Right now, PABs have tax-free status, but that status may disappear as soon as New Year’s. That’s because the tax plan passed by the House of Representatives cuts it, while the Senate plan keeps it. The two sides are battling it out right now.

Here’s what’s getting lost in the noise: no matter what happens, the outcome will be good for municipal bonds.

First, if PABs’ tax-free status disappears, it would likely lower the number of municipal bonds in the market. But the number of income-hungry investors is growing by the day, so demand will rise, boosting the value of already-issued muni bonds.

And if PABs’ tax-free status stays, a lot of anxiety will evaporate from the market, and risk-averse investors on the sidelines will creep into muni bonds.

It’s a rare win-win situation, which is why you should consider municipal bonds right now.

But what’s the best way to buy them? As I wrote in a September 5 article, I prefer buying munis through closed-end funds (CEFs), for two reasons:

- CEFs’ dividends are higher than those of muni ETFs and mutual funds, and

- CEFs often trade at big discounts to their net asset value (NAV, or the market price of the fund’s portfolio if it liquidated everything).

Since my article recommending muni-bond CEFs is still pretty recent, I was a bit surprised to see Barron’s basically write the same thing just a couple weeks ago.

But I’m not upset; I’m happy to see Barron’s jump on the CEF bandwagon!

Like me, Barron’s likes the fact that municipal bond CEFs yield more and trade at a discount, which not only gives investors a bigger income stream now but bigger total returns over the long term.

At our CEF Insider service, we did our own analysis and found that the majority of muni-bond CEFs outperformed municipal-bond ETFs and mutual funds over a long time horizon, and over 80% of muni CEFs have outperformed their benchmark index since their IPO.

Another in-depth analysis of CEFs, by Jun Zhu of Leuthold Group (a firm that sells research to hedge funds and other big investors) found pretty much the same thing.

The key to outperforming with a muni CEF is the fact that CEFs often trade at discounts. Because of that, investors can buy shares trading at big discounts from scared investors who sell at the same time. “This wealth-transfer mechanism is not possible in open-end funds, as those prices are almost always equal to NAV,” Zhu concludes of this process.

The end result? Muni investors using CEFs outperform by a wide margin.

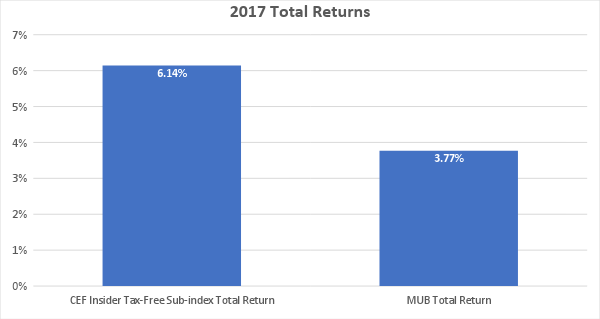

That’s exactly what we’ve seen in 2017. If we look at CEF Insider’s Tax-Free Sub-Index, which tracks the returns for all municipal bond CEFs, and compare it to the benchmark iShares National Muni Bond ETF (MUB), we see that the CEFs are outperforming by almost double:

This confirms Zhu’s study and what we at CEF Insider have also seen in the past: if you want to buy municipal bonds, closed-end funds are the best way to do it.

The One Muni-Bond Fund You Need to Buy Now

My favorite muni-bond CEF trades at a ridiculous 7.5% discount to NAV—way lower than its historical average—while handing us a gaudy 5% dividend yield.

And that yield doesn’t account for this fund’s tax-free payout!

That’s a much bigger payout than you’d get by purchasing munis on their own. And it leaves the cheapskate 2.2% yield on MUB, the go-to muni index fund, firmly in the dust.

But this unusual 7.5% markdown is on borrowed time because, as I said earlier, once the herd looks beyond tax reform, they’ll realize they’re missing out on a big dividend here and stream back in, slamming that discount shut and driving the share price higher.

And keep in mind that this is a small fund, with a market cap of just $2.1 billion, so it only takes a few new buyers to nudge its price higher. That creates a “feedback loop” as other folks spot the fund’s narrowing discount and jump in, too.

I’ve seen it happen again and again over my career as a CEF analyst. And the trigger for this particular pick is sure to be the end of the PAB debate, which I expect to come before January.

That means you need to make your move now. To get the name of this fund and all 13 holdings in my CEF Insider portfolio (average yield 7.6%), simply CLICK HERE. When you do, I’ll also give you 3 Special Reports revealing my top 4 CEFs for 2018, my complete CEF investing strategy and more.

Recent Comments