Plenty of income investors say they are in it for the dividends. But they mistakenly fixate on erratic (and irrelevant) charts like these:

This Chart Will Cost You Money…

Instead of charts with actionable information – like these:

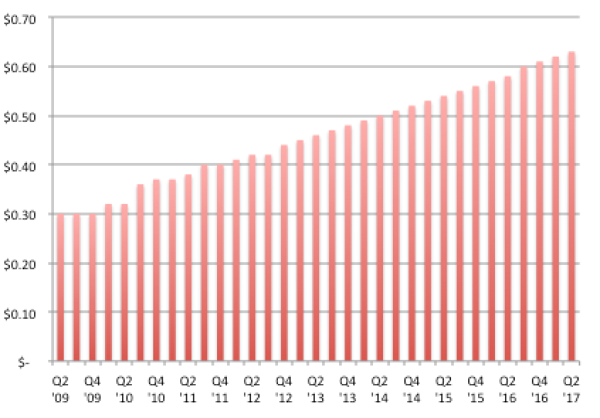

… While This One Will Make You Wealthy

The first chart was price-only, a source of agony for many investors. While the second was quarterly dividends, with this example representing the perfect passive income stream for any retiree.

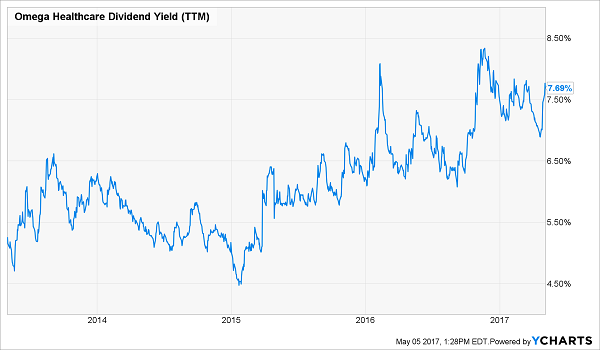

The latter is often available at a discount because the former – the share price of Omega Healthcare (OHI) – keeps its “ticker watchers” busy. Even though price has gone nowhere lately, it’s been quoted as high as $38 and as low as $28 per share. That’s a big range for a stock that does nothing except raise its dividend every single quarter.

When a stock trades sideways with an ever-rising dividend, its current yield rolls higher quickly. That’s exactly what’s happening with OHI:

A Bull Market in Current Yield

And don’t be fooled by the “mere” 7.7% trailing yield that most financial websites will quote you. Their dividend information is living in the past. Shares will pay 8%+ in the year ahead (thanks to four more payout hikes in the next 12 months).

Any serious income investor should be considering a stock like this. But most first-level types can’t get past the price fluctuations and headline concerns. Let’s look at the types of questions investors should be asking themselves when an 8% dividend grower like this is available.

Is the Current Dividend Secure?

An 8% yield in a 1% world is fantastic. A payout of this level will provide a floor on any stock (or fund) price.

OHI will generate $3.40 to $3.44 per share in AFFO (adjusted funds from operations) this year and pay just $2.54 in dividends. That’s a payout ratio less than 75%, which is quite comfortable for a REIT (real estate investment trust) and well below management’s target of 85% or less.

OHI’s current payout is no problem.

Will the Dividend Keep Growing?

If you’re a regular reader, you know I believe dividend growth is the most powerful force in the investment universe. As fantastic as a secure 8% yield is, a growing payout of this magnitude makes OHI a potential “income unicorn.”

But we can’t simply look in the rearview mirror at the firm’s amazing history of 19 consecutive quarterly dividend raises. This is the mistake most Dividend Aristocrat fanboys make – they chase past payout performance and suffer when future growth stalls.

Tomorrow’s dividend raises are driven by tomorrow’s cash flows. Demand for OHI’s skilled nursing facilities (SNFs) should remain strong in the years ahead thanks to demographics (and 10,000 baby boomers turning 65 every day). Meanwhile industry supply is actually shrinking – amazingly, there are fewer SNFs in the U.S. today than there were 10 years ago.

OHI spent a modest $8 million purchasing new facilities in the first quarter, with another $30 million invested in renovations. These low numbers were actually knocked – how quickly people forget last year’s $1.3 billion in new investments are still being digested!

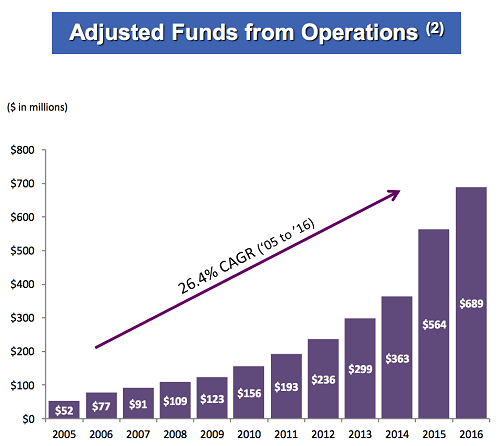

Bottom line, there’s no reason doubt a management team that’s compounded absolute AFFO by 26% annually since 2005:

What About Interest Rates?

Here’s where daily ticker watchers get fooled. On a given day, if the 10-year Treasury rate is up, OHI is probably down:

An Apparent Inverse Relationship

But this isn’t OHI’s first rate hike rodeo. From 2003 to 2006, the 10-year yield jumped from 3.1% to 5.3% – and the healthcare REIT rewarded investors with an amazing 449% total return over that 3-year period!

449% Returns During Last Rate Hike Rodeo

Thanks to overblown rate worries, it’s the best time to buy REITs since 2009. Take advantage of rallies in the 10-year rate to purchase shares in your favorite REIT at a short-term discount.

Finally, What About Politics?

Should we be buying OHI? It’s incredibly cheap, trading for less than 10-times AFFO. As you might expect, there are more than just rate worries weighing on shares.

Medicare and Medicaid are the stable payer sources for the majority of patients in OHI facilities. They’re run by the government, so there’s always something to worry about. And right now is no different, with the Republicans once again attempting to repeal Obamacare.

Now out of respect for my paid Contrarian Income Report subscribers, I can’t reveal here whether or not OHI meets the strict criteria for my 8% “No Withdrawal” Portfolio – which has quickly gained acclaim as the best investing strategy for retirement.

Reason being, the high (and secure) 8% yields in my portfolio provide you with meaningful income, so that you can live off your dividends alone, and not worry about day-to-day ticker action.

If you have a $500,000 portfolio, this strategy will provide you with $40,000 in annual income and keep your capital intact. If you have a million bucks, that’s $80,000 per year.

And to be honest, you’ll probably grow your capital too. We only buy high quality stocks and funds when they are:

- Paying 7% or 8% or better in yield,

- Trading at a steep discount to their intrinsic value,

- And being unfairly punished by headline worries that our research debunks.

My three favorite recession-proof REITs are a great example of the secure high yield, high upside firms we own. And I’d love to send you my full analysis, including stock names, tickers and buy prices. Click here for a risk-free look at my entire 8% No Withdrawal Portfolio.

Recent Comments