It sounds hard to believe, but sometimes a dividend hike can be dangerous. In fact, when it comes to closed-end funds (CEFs), sometimes the worst thing you can see is a fund with a generous payout, a very high yield and a history of dividend increases.

It’s true!

And today I’m going to show you how this tough-to-spot CEF trap can slash your payouts (and your nest egg). Then we’ll dive into one fund that looks like a healthy dividend grower—but is, in fact, anything but.

A Hidden Danger

Make no mistake: the hazard I’m going to show you now is real. It exists because of overzealous fund managers, who give in to the temptation to boost dividends just to impress investors.

That can set off a disastrous chain reaction as CEF buyers respond to these dividend hikes with a rally, driving up the market price and cutting the fund’s discount to NAV. The result is a massive overvaluation—and a hard fall when the fund is inevitably forced to cut payouts.

Take a Pass on This CEF’s Dividend High-Wire Act

To show you what I mean, consider the fund I want to warn you about today: the RiverNorth Opportunities Fund (RIV), a corporate-debt fund that’s gotten a lot of favorable attention from investors, thanks in part to the 15.4% yield it was recently offering (it’s now paying 12.3%; I’ll tell you why below).

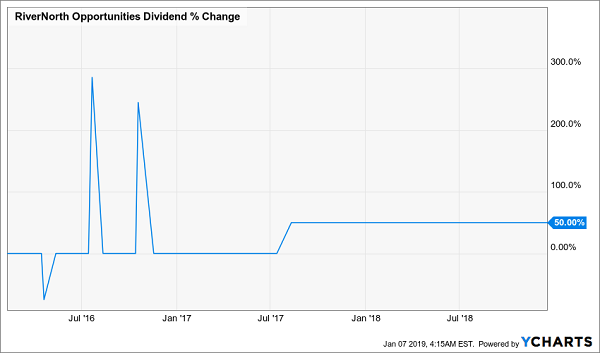

But that wasn’t the only reason investors fell in love with RIV. This chart was another:

A Too-Good-to-Be True Payout

Dividend increases on this scale aren’t common in CEFs (especially those already boasting double-digit yields), and big hikes to the regular dividend plus huge special payouts (represented by those spikes in 2016) are unheard of. So you can see why RIV would look like a godsend to income-starved investors.

But the trouble is, if those dividend increases don’t come with higher capital gains and investment income, they can spell disaster for a CEF. And that’s the storm that’s brewing with RIV.

Before I get to the fund’s many fundamental problems, let me point out another issue with RIV: management’s shortsighted, overly aggressive dividend policy.

At the start of 2019, RIV announced it would set dividend payouts at 12.5% of the fund’s NAV, meaning that RIV must earn more than 12.5% to pay for management fees (currently 1.4%) and dividend payouts. If it fails, the fund will need to eat into its assets, resulting in a death spiral.

Can RIV earn such a large return? While anything’s possible, the fund’s 5.7% annualized return on its NAV since its inception three years ago doesn’t bode well, but what’s worse is the fact that its return has worsened substantially in recent months:

RIV Suffers a Major Hiccup

Having a bad 2018 isn’t worrisome on its own—after all, everything except cash fell last year—but RIV’s poor performance becomes much more of a concern when you combine it with its dividend policy. By not cutting distributions in 2018, when the fund could have been using that extra cash to reinvest in temporarily discounted assets, RIV’s management team let an opportunity to get more future income pass by.

Instead of prudently managing its access to cash, RiverNorth decided to increase its investments in the temporarily depressed market of late 2018 with a rights offering—basically an offer only to existing stockholders to buy newly issued shares in RIV at a slight (5%) discount to the fund’s market price. While this increased the fees RIV’s managers collect, it was also a more expensive way to reinvest in a temporarily weak market than cutting the dividend slightly.

And that’s not even the worst thing with RIV.

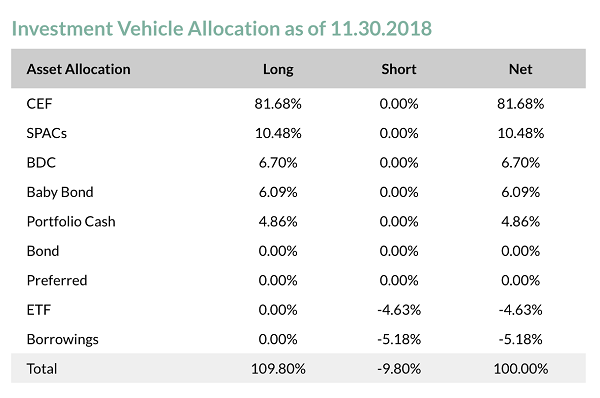

For much of its short history, this fund has done what any retail investor could easily do: invest in a bunch of CEFs and ETFs. With 81.7% of its assets in CEFs, RIV is best thought of as a fund-of-funds, which introduces two problems.

Source: RiverNorth Capital Management

The first, and perhaps best-known, problem with the fund-of-funds approach is how it compounds fees. Not only are you paying RIV’s fees, but RIV is also paying fees to the funds it holds. And you’re ultimately paying those fees, too, since they come out of RIV’s performance. This is why the fund-of-funds approach has been losing popularity fast on Wall Street.

The second problem is specific to CEFs: overleverage. Since RIV borrows money to invest (fortunately its leverage is currently just 9.8%), and since RIV invests in CEFs that also use leverage, the borrowing power of this fund is compounded. That’s works well in good years, because it can compound returns, but the much bigger risk is that a really big market move could result in forced selling during a bear market—or the fund outright blowing up and being worth zero.

With such risks involved, you’d be wise to avoid RIV if you’re on the lookout for a high income stream.

Oh, and before we leave RIV behind, a postscript: the fund’s new reality started to set in late last week, when management said it would do what it should have done long ago: cut its dividend—in this case by by 19.1%. RIV’s new dividend yield is a still-high 12.3%, but there are more cuts to come, since this fund’s payout promises are still unsustainable, no thanks to its fund-of-funds setup and poor capital allocation strategy.

Yours Now: My 4 Safest 7%+ Dividends for 2019—and Beyond

Steering around the deadly RIVs of the world—and guiding you to the many safe 7%+ cash dividends waiting for you in CEFs—is what I do day in and day out at my members-only CEF Insider service.

In fact, I recently unveiled my 4 SAFEST 7%+ dividends you can buy right now—and I’ll GIVE you the names of these retirement-saving powerhouses when you click right here.

These 4 bargain funds—which I’ve dubbed “pullback-proof” dividends—are rock-solid and growing for all the right reasons: management is making money hand over fist, so much so that it’s practically begging us to take it off their hands!

So why do I call these 4 CEFs “pullback proof”?

Because each one trades at a totally unheard-of discount to NAV—a crucial measure of safety that gives us two “must-have” strengths:

- Crash protection: When the market falls out of bed, these 4 funds’ discounts cushion the blow—and let us pocket their rich 7%+ payouts without losing sleep at night, and …

- Unbeatable upside, as these same discounts set these 4 funds up “spring loaded” gains when stocks soar.

I’m one of a small handful of analysts in the world devoted 100% to high-yield CEFs (and I’ve been putting my own personal cash in these funds for years). I’ve spent hours sifting and analyzing to come up with these 4 “best of breed” funds, and I can tell you this:

These are precisely the kind of investments you need to own now, when the Dow can whipsaw 2% or more on any given day.

Simply click here now and I’ll give you everything you need to know about these 4 battle-hardened, cash-rich CEFs: names, ticker symbols, buy-under prices and my complete research, so you can kick-start your own reliable 7%+ income stream today.

Recent Comments