America’s richest investors are earning reams of tax-free income from an investment most people ignore, and today I’m going to let you in on it.

In fact, it’s hardly a secret at all. It’s just sitting there, in plain sight. And it’s very popular with the multi-millionaires and billionaires among us for one reason: as their investments throw off an ever-rising stream of dividends and capital gains, these folks get bumped into higher and higher tax brackets.

That hardly seems fair—and it feels like double taxation. But that’s how the tax system works. And this is where these dull-as-dishwater investments come in.

Income the IRS Can’t Touch

I’m talking about municipal bonds.

In a nutshell, municipal bonds are never taxed by the federal government and are usually not taxed by most states, so they give you tax-free income that boosts your monthly cash flow without kicking you up into a higher tax bracket.

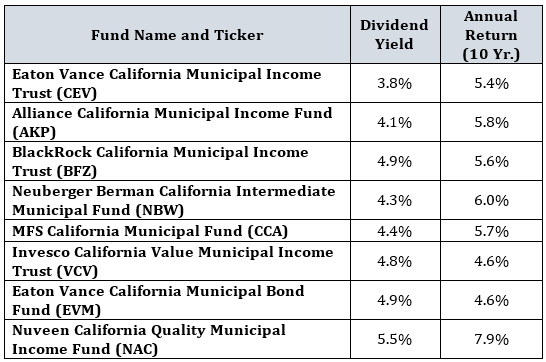

In a moment, I’ll show you 8 municipal-bond funds from America’s biggest (and wealthiest) state that yield up to 5.5% today—tax-free. I’ll also name one fund-management company that’s a big name in the municipal-bond-fund business, but their funds are hopelessly overvalued.

Buy into them and you risk locking yourself in for years of meager returns—or worse.

At this point you may be wondering why I made the switch from talking about municipal bonds to municipal bond funds there.

The answer is simple: much as I love municipal bonds, their yields aren’t that great, and the safer the bond, the lower the yield.

Consider California. America’s wealthiest state in terms of GDP has been improving its budget over the last half-decade, so the interest rate the state has to pay on the bonds it issues has gone down dramatically. Right now the average California municipal bond yields just 1.7%—that’s less than a US Treasury bond and the rate of inflation!

But there are a number of bond funds that invest in these high-quality California bonds while paying much higher yields—as high as 5.4%! And remember, that’s tax-free. Put $100,000 in any of these funds and you’ll get $450 per month in completely tax-free income.

Your best choices are high-yielding closed-end funds (CEFs), which have some of the best annualized returns out there.

The downside is that muni-bond CEFs are finding their way onto everyday investors’ radar, so a lot of them are moving into overbought territory, and getting riskier every day.

For instance, consider the PIMCO CA Municipal Income III Fund (PZC); I wrote about this fund a month and a half ago, noting that its price plummet was unavoidable because it was trading at an absurdly high premium to its net asset value (NAV, or the value of its underlying assets).

Here’s what happened:

PZC’s Big Name Can’t Save It

That sudden crash in price is not what you want in an asset that’s supposed to be as safe as a municipal bond.

Fortunately, there are eight funds on the market that offer more sustainable income than this fund and better returns, too.

While PZC has had an annual return of 4.4% over the last decade while paying a 4.9% dividend, here are some funds with better returns and similar or even higher dividends:

So how can these funds perform so much better than PZC—and why aren’t investors choosing them over the PIMCO option?

Well, that’s a funny story.

To understand why PIMCO’s California bond funds are a bad deal (PZC is just one of many the company offers), you need to know a little bit about PIMCO.

Short for Pacific Investment Management Company, PIMCO is based in Newport Beach, California, where it was established by UCLA alum Bill Gross. Over the last few decades, the firm has exploded to manage nearly $1 trillion for investors.

A big part of the reason why is that PIMCO has made an aggressive marketing push throughout California. Because of their accessible HQ in Newport Beach and the connections PIMCO has with the ultra-rich of California, the company has an easy market in which to sell its products in its home state. This also means its funds tend to be overbought and offer little extra value.

Meantime, other management companies have similar or better long-term performance in their funds, but since they’re not based in California, they can’t compete with PIMCO when it comes to marketing to investors.

That means these funds are often undervalued relative to the fund’s actual asset value. For instance, you’d need to pay $1.10 for $1.00 of assets if you bought PIMCO’s PZC—but $1.00 of assets costs just $0.89 with the Eaton Vance CA Municipal Income Fund (CEV)!

The bottom line? There are lots of muni-bond CEFs out there set to hand you 4%+ tax-free income and strong gains, too.

How about a growing 7.4% dividend and 20% upside?

I’ve just uncovered 4 other funds that tick off ALL my boxes for the perfect investment: a 7.4% average payout, steady dividend growth and 20%+ price upside.

How do I know they’re about to soar?

Because they all share one blaring buy indicator: unlike the PIMCO funds, which often trade at ridiculous premiums to NAV, these hidden gems trade at big discounts.

In other words, these 4 funds are geared up for HUGE price gains! And you’ll be collecting that hefty 7.4% income stream while you watch them take off.

Take my No. 3 pick, which I’ll reveal to you in a new FREE report you can download right here.

This all-star fund owns blue chip stocks like Google (GOOGL), Apple (AAPL), American International Group (AIG) and MasterCard (MA).

But there’s more.

Their top-flight management team then adds its “secret sauce”: a powerful yet conservative income strategy that delivers a far higher yield than you’ll find on any mainstream bond or stock out there: a rock-solid 7.4%! (I’ll tell you exactly how their proven approach works in my NEW free report.)

And as I just mentioned, this income wonder trades at a ridiculous discount to its true value—but that won’t last long!

Let’s grab a piece of the action now, before the market comes to its senses on this one. CLICK HERE and I’ll tell you all about this winning CEF and my 3 other top high-yield picks.

Recent Comments