Many investors mistakenly believe that the world of private equity and its home-run potential are hopelessly out of reach. Privately held PE firms are difficult to access and often require seven-figure sums to start. Plus the handful of publicly traded PE companies are organized as limited partnerships – which means a hassle come tax time.

But there’s a promising group of easy-to-buy private equity firms hiding in plain sight: business development companies (BDCs).

And BDCs are dividend behemoths. In fact, I’ll highlight three today paying up to 9%!

Business development companies are the lifeblood of American small business, providing financing to small and mid-sized business in many instances when banks and other financiers consider the risk to be too great. Like real estate investment trusts (REITs), BDCs were designed to stimulate a particular type of investment. As a result, they have the same mandate – to distribute at least 90% of their taxable income as dividends to shareholders.

BDCs are also the easiest route that you and I have to the sizable, diversified returns of this alternative investment. Unlike Blackstone Group LP (BX) or KKR & Co. LP (KKR), there’s no complicated K-1 to deal with – a regular 1099 will do.

There are numerous benefits to investing in BDCs, including their often sky-high yields and the fact they’re mostly shielded against rising interest rates. But like all investments, the carton can come with a few cracked eggs.

Today, I want to introduce you to three notable business development companies. Two of these enticing BDCs are actually trouble right now, while just one is a truly quality high-yield opportunity.

Ares Capital Corporation (ARCC)

Dividend Yield: 9%

Price/NAV: 1

Ares Capital Corporation (ARCC), which has been around since 2004, is no small potato in the world of BDCs, sitting around $7 billion in market capitalization. Ares targets companies with “a history of stable cash flows, demonstrated competitive advantages and experienced management,” and isn’t afraid to tussle with most industries, though it has preferences for certain industries, including business, healthcare and information technology services, as well as consumer products and light manufacturing.

All told, ARCC has some 300 investments, but to get an idea of the diversity you’d have indirect access to, holdings include church-focused software provider Ministry Brands, residential and commercial laundry solutions company Spin Holdco scuba diver training and certification servicer Surface Dive.

The diversification is nice, and at 9% currently, so is the yield. But the dividend itself isn’t exactly on solid footing at the moment.

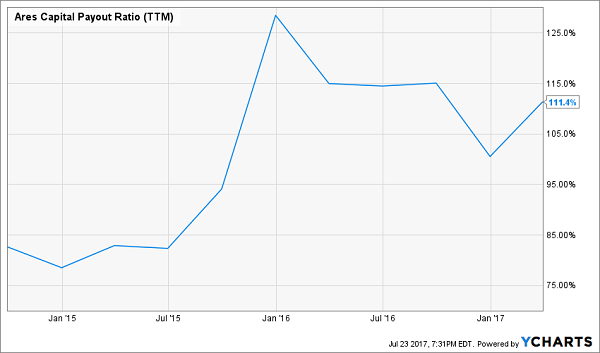

In May, Ares Capital delivered a disappointing earnings report that was enough to send shockwaves throughout the rest of the BDC industry. Core earnings of 32 cents per share were far shy of estimates, and net interest income of 22 cents per share was off by nearly 40%. Both figures are less than the company’s 38-cent dividend.

Of particular worry is Janney analyst Mitchel Penn’s assertion that ARCC’s dividend payout for the full year will come out to more than its earned income. And considering that the stock trades for no discount whatsoever, there’s no reason to take a flyer on Ares.

Ares Capital’s (ARCC) Dividend Is Rich, But Overextended

Main Street Capital Corporation (MAIN)

Dividend Yield: 5.8%

Price/NAV: 1.72

Main Street Capital Corporation (MAIN) leans toward the other extreme.

This BDC invests in companies with $3 million to $20 million in EBITDA and $10 million to $150 million in revenues, requiring similar criteria as Ares, such as competitive advantages and seasoned management. And it does so through several avenues – senior secured debt, preferred equity and common equity, among others.

It’s similarly diverse, too, investing in the likes of for-profit educator Ameritech College, self-service key-duplicating kiosk company MinuteKey and technological pricing solutions provider Zilliant.

I have little complaint with the company’s operational performance, with assets slowly ticking in the right direction, and actual growth in the dividend over the past couple years.

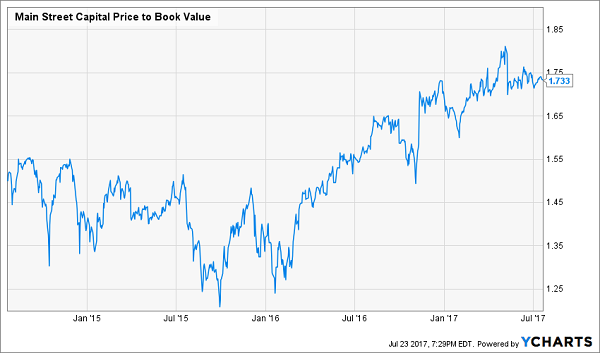

But MAIN shares have gotten way ahead of themselves, trading for a 72% premium to the company’s NAV! That’s among the highest overvaluations in the industry, and a reckoning just waiting to happen. That, combined with a sub-6% dividend that also ranks among the industry’s worst, means that while Main Street might be a good company, it’s too expensive and doesn’t offer enough income to consider right now.

Typically Premium-Priced Main Street Capital (MAIN) Has Gotten Out of Hand

Gladstone Investment Corporation (GAIN)

Dividend Yield: 8.1%

Price/NAV: 0.95

With Gladstone Investment Corporation (GAIN), we finally have our Goldilocks.

Gladstone is actually part of a family of public investment vehicles that also includes Gladstone Capital Corporation (GLAD), Gladstone Commercial Corporation (GOOD) and Gladstone Land Corporaiton (LAND).

Gladstone typically tries to invest at a 75%-25% debt-to-equity blend, with the biggest concentrations of investments going toward the mouthful “Home and Office Furnishings, Housewares, and Durable Consumer Products”; diversified/conglomerate services; and chemicals, plastics and rubber companies. Portfolio companies include the likes of Ag Trucking, Club Car and E-Z-Go golf cart distributor Country Club Enterprises, and Westland Technologies, which provides radar and acoustic absorption tiles to U.S. Navy vessels.

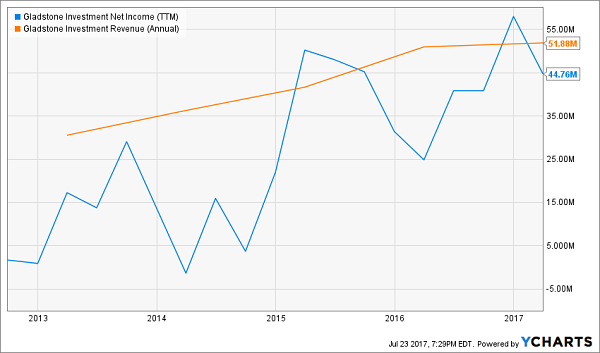

Gladstone Investment (GAIN) Delivers Greenbacks AND Growth

And GAIN checks off a lot of boxes. Its dividend is ample at just north of 8%, and that comes in a monthly payout that was hiked earlier this year to 6.4 cents. Meanwhile, its price-to-NAV represents a 5% discount at the moment – despite a great 12% capital gain in 2017 that even has the S&P 500 beat!

Among these three BDCs, GAIN has the ideal mix of quality and value.

Retire in Style With 12% Annual Returns For Life!

I can’t stress this enough: It’s vital that you secure high yields like the kinds that Gladstone Investment offers, or you’ll be doomed to a second-rate retirement full of skimping and cutting corners to get by.

But if you want to make it through retirement fully funded and without a care, you also need dividend growth and capital gains potential – the formula it takes to deliver 12% in safe annual returns.

Wall Street is littered with high-yield death traps whose payouts are just a couple years away from vanishing. It’s also full of blue chips that offer loads of safety, but no room for growth and dividends that simply aren’t enough to pay the bills in retirement. That’s why I’ve been buried in data for months now, tracking down the kind of portfolio that offers the high current yield, dividend growth track and capital gains potential possible to reach double-digit returns.

The result is my “12% for Life” portfolio.

This set of stock picks will reap at least 12% in annual returns – which is what you need to ensure the kind of no-worries retirement you’ve been busting your hump to achieve for the past few decades. And as you might imagine, this isn’t your garden-variety dividend portfolio.

Forget popular pundit picks like Exxon Mobil, Coca-Cola or any other “safe” blue chips that offer no growth and less-than-generous yields. Instead, you’re going to find …

- A stock that has already boosted its dividend payments more than 800% over the past four years, and has at least another decade of double-digit growth left in the tank!

- A “double threat” income-and-growth stock that rose more than 252% the last time it was anywhere near as cheap as it is right now!

- A 9%-plus payer that raises its dividend more than once a year, and will double its payout by 2021 at its current pace!

This set of no-doubt dividend picks combines the best aspects of numerous types of investment strategies – income, growth and even portfolio protection! All told, these are seven investments that can return 12% annually, which is enough to double your portfolio in six years. It also is built to survive downturns like 2008-09, which wiped out trillions of dollars in wealth and shattered the retirement plans of countless Americans.

And best of all: It provides three times more income than most retirement experts say you need!

Pay your bills in retirement from dividend income alone and have enough left over for all the extras – a new patio, a timeshare in Palm Beach, an all-inclusive European cruise. And most importantly, you can continue building your nest egg, which offers downside protection against life’s ugly surprises.

Let me show you how to earn the double-digit returns you need to enjoy retirement at its fullest. Click here and I’ll GIVE you three special reports that show you how to earn 12% for life. You’ll receive the names, tickers, buy prices and full analysis for seven stocks with wealth-building potential – completely FREE!

Recent Comments